ScholarMatic: Explanation & Answer

Your ready answer from a verified tutor is just a click away for as little as $14.99

Click Order Now to get 100% Original Answer Customized to your instructions!

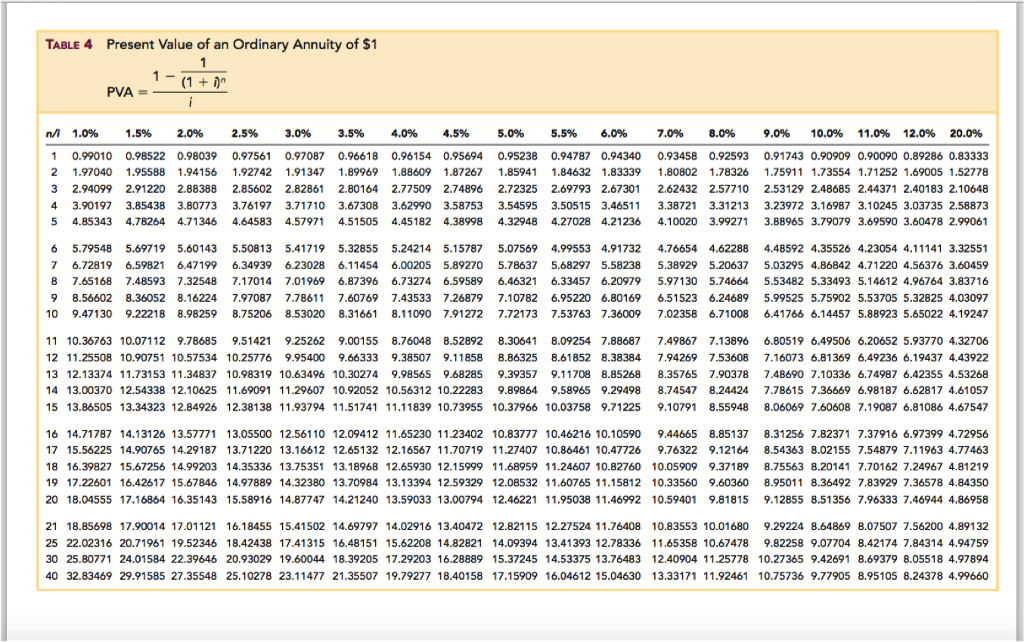

Note: You MUST use the Time

Note: You MUST use the Time

Value of Money factors (which are provided in the in-class slides)

to complete this assignment. Answers determined using a financial

calculator will not be accepted.

On January 1, 2016, Dudley Company issued $800,000 of five-year,

6% face value bonds that pay interest semi-annually each June 30

and December 31. The bonds were issued to yield an 8% return.

Required:

1. a. Prepare the journal entry to

record the issuance of the bond.

Prepare an amortization table for all years of the bond’s life

to record the amortization of the premium or discount, using the

effective interest method.

Prepare the journal entry for the first two interest payments,

assuming that Dudley uses the effective-interest method to amortize

the premium or discount. (Your figures will come from the

amortization table).

Prepare the journal entry for the first interest payment,

assuming that Dudley uses the straight-line method to

amortize the premium or discount.

Assume that, on December 31, 2018, Dudley redeemed all of the

outstanding bonds at 103. Prepare the journal entries for this

transaction. Use your amortization tables to help you determine the

carrying value of the bond at the time of redemption.

Repeat requirements “1a” through “1d” assuming that the bonds

issued had a stated rate of 10% instead of 6%. (The yield is still

8%).

Looking at your amortization tables for both scenarios, does

your INTEREST EXPENSE increase or decrease each period when you

amortize a discount? What about when you amortize a premium?

Looking at your amortization tables for both scenarios, does

your CARRYING VALUE increase or decrease each period when you

amortize a discount? What about when you amortize a premium?

Looking at your amortization tables for both scenarios, what do

you notice about the AMOUNT OF AMORTIZATION (the difference between

your interest paid and the interest expense) each period? Does it

increase or decrease each period when amortizing a discount? What

about when you are amortizing a premium?

Looking at your amortization table, when amortizing a premium

using the effective interest method, is your interest expense in

the earlier years greater than or less than it is when amortizing

your premium using the straight-line method? What about in later

years?

Looking at your amortization table, when amortizing a discount

using the effective interest method, is your interest expense in

the earlier years greater than or less than it is when amortizing

your discount using the straight-line method? What about in later

years?

ScholarMatic: Explanation & Answer

Your ready answer from a verified tutor is just a click away for as little as $14.99

Click Order Now to get 100% Original Answer Customized to your instructions!